Being in debt is normal — statistically speaking.

But there’s a difference between manageable debt and unmanageable debt.

And you’ll know if you have unmanageable debt if:

- You don’t know how much you owe.

- You’re not paying off your statements in full each month.

- You’re suffering psychologically from it (e.g., losing sleep, avoiding emails/phone calls from bank).

And unfortunately, there are a lot of people out there who want to take advantage of this. These are organizations that prey on people in debt in order to get money out of them — keeping them in debt longer.

Fortunately, there IS hope. Below I’ve outlined a system to help you reduce debt quickly and also give you a look into debt reduction companies so you can make the best choices for you.

What is debt reduction?

Debt reduction is taking proactive measures to cut down the money you owe to creditors. This includes things like:

- Credit cards

- Student loans

- Car loans

- Mortgages

- Utility bills

- Rent

And there are actually debt reduction services out there that’ll help you with this. They’ll work with your creditors to either A) consolidate your debt, B) negotiate with your creditors to lower your payments, or C) a combination of both.

Note: Debt consolidation is the process of using one loan in order to pay off all of your debt. That loan has a lower interest rate than your debt. So in theory you’ll end up paying less because you’re not paying as much in interest.

On the surface, they can seem like a gift from heaven. Angels sent by God to help lift you out of debt forever. What could be better?

Well, there are a LOT of pitfalls that can come with them.

I’ve talked about this before in my article about debt consolidation — but the short of it is this: Many of these companies prey on people in debt in order to get money out of them for as long as they can.

There are a lot of issues with this, but the three biggest ones are:

- You’ll be in debt longer. Even the scammiest consolidation services will be able to give you a lower interest rate on your loan. However, they often protract your loan term (the length of your loan), meaning you’ll be in debt longer and end up paying more even with lower interest rates.

- You might lose a BIG asset. If you put your car or home down as collateral and fail to make payments, your debtors are within their rights to repossess those assets. Losing a car could mean your livelihood is at stake if you commute to work. And having a house taken away from you could mean homelessness.

- Your credit score will drop. 15% of your credit score is how long you’ve held onto a line of credit for. That means if you pay off a bunch of credit and take on a single big loan, you’re going to see a drop in your score. That drop only gets bigger with the more lines of credit you close.

That said, there ARE good debt reduction services out there. The trick is to find a good one that’ll fight for you — instead of squeeze you for all the money you have.

How to find a good debt reduction service

If you want to find a good debt reduction service, look for a non-profit.

These are 501(c)(3) organizations that help provide debt relief through things like:

- Consolidation

- Credit/debt counseling

- Negotiating lower interest rates or total payment with your creditors

Since they are non-profit organizations, these debt reduction services are funded through grants and donations — meaning they’ll cost you little to nothing to use their services.

There are still scammers to be wary of (even in the non-profit world). So to make sure you find a reliable debt reduction service, you’ll need to look out for a few things:

- Fees. Yes, you read that right. Reputable non-profit debt reduction services will charge you a fee. These are typically monthly maintenance fees that are relatively low cost. Note: A good non-profit will work with you if you cannot afford it. Some will even waive the fees entirely for you.

- Non-profit status. “Well, no duh,” you’re probably saying. But the reality is a lot of scammers pretend they’re non-profit in order to take advantage of people’s goodwill.

ACTION STEP: Find 5 – 10 non-profit debt reduction services.

Spend the next week calling them and asking them about their fees, proof of their non-profit status, and what they can do for you.

A good non-profit will spend about an hour on your consultation. Beware of any organization that wants to take your money and put you into a plan right away. They are NOT looking out for your best interests.

How to get out of debt IWT style

Below is our process to help you eliminate debt for good. We go more into this system in our article on how to get out of debt fast — but I’ll give you a solid rundown of it below so you can get started as soon as possible.

Because if there’s one important thing when it comes to getting out of debt/investing/saving/earning/anything finance related, it’s this: It’s best if you do it early, often, and consistently.

Let’s get started.

Step 1: Discover exactly how much you owe

A lot of people in debt don’t actually know how much they owe.

It all boils down to human nature. Debt is a bad thing. Society looks down on people who owe exorbitant amounts of money. So people end up feeling guilty about their debt.

So what do we do? One of two things:

- Blindly pay the minimum amount toward bills with no strategy.

- Not pay at all because we’re paralyzed by our debt.

You play right into the creditor’s hands when you do this. They’ve designed the system so it’s easier for you to just send in the minimum payment or avoid paying entirely. When you do this, they end up getting MORE money.

You need to fight against this BS. And the first step in doing that is finding out exactly how much you owe. In the end, you’ll probably find that it’s not as bad as you anticipated.

ACTION STEP: Find out how much you owe across all of your debt.

Spend the next hour finding out how much debt you owe. This means calling up your credit card companies or digging up a recent statement. Logging onto your student loan portal to see how much you owe. Or emailing your mortgage lender. Whatever it takes to find out how much you owe.

Add up all of the numbers on a spreadsheet and you’ll have a solid idea of how much you owe.

Once you do that, congrats! You’ve taken the hardest and first step in getting out of debt.

Here’s a handy spreadsheet template you can use to calculate your debt.

|

DEBT |

TOTAL OWED |

APR |

MONTHLY MINIMUM PAYMENT |

|

Credit card A |

$X |

X% |

$X |

|

Credit card B |

$X |

X% |

$X |

|

Student loan |

$X |

X% |

$X |

By finding out exactly how much you owe, you can start to strategically approach taking down your debt.

Step 2: Decide what to pay first

Now you need to ask yourself: Which debt should I pay off first?

And there are a lot of different ideas on how this should be approached.

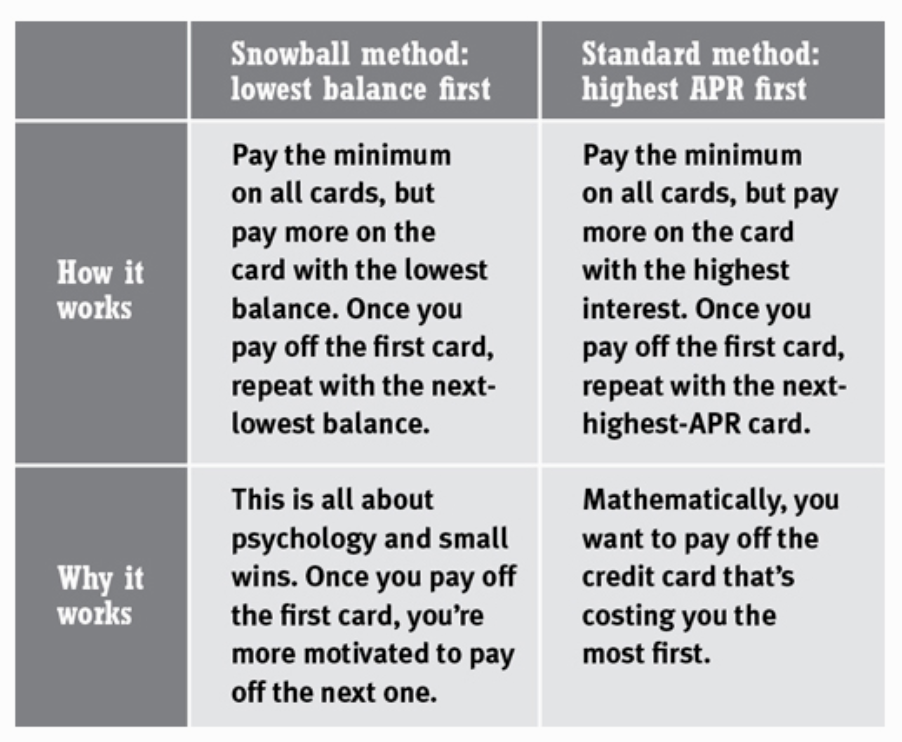

The standard method involves paying the minimum on all debt, but pay more money to the loan with the highest APR because it’s costing you the most.

Dave Ramsey famously touts his Snowball Method of getting out of debt. This involves paying the minimums on all of your debt, but paying more money to the card with the lowest balance first (i.e., the one that will allow you to pay it off the quickest).

This is a source of fierce debate in debt reduction circles. Technically, this method isn’t the most efficient way to approach your debt since the debt with the lowest balance doesn’t necessarily have the highest APR. Psychologically, it’s very rewarding to see one debt paid off. That’s why it’s the one I suggest.

For more on this, check out my video below.

ACTION STEP: Choose a debt reduction strategy.

It doesn’t actually matter too much which method you choose. The important thing is for you to choose one.

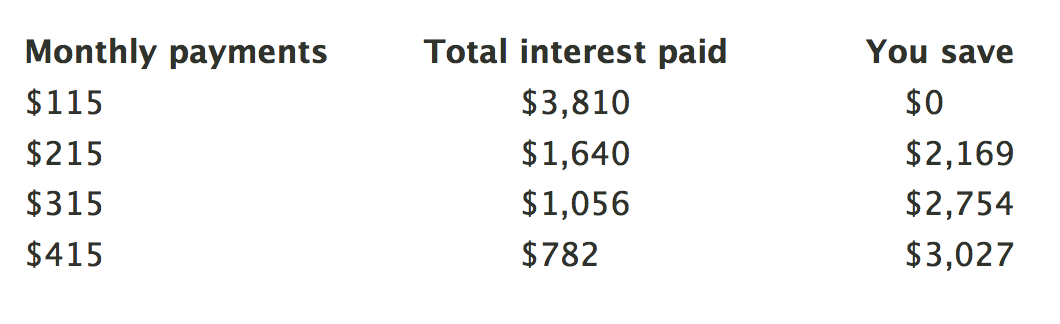

Pro tip: When it comes to your student loans, you can actually save thousands of dollars each year — by paying down your debt more each month.

Let’s say you have a $10,000 student loan, at a 6.8% interest rate, and a 10-year repayment period.

If you go with the standard monthly payment, you’ll pay around $115/month.

But check out how much you can save per year if you paid just $100 more each month:

Even $20 more per month can save you huge amounts of money.

See for yourself by calculating your savings using this calculator.

Step 3: Negotiate your APR to save thousands

I’m a huge fan of taking 50/50 odds if the upside is big and it only takes five minutes of my time.

That’s why I love negotiating my interest rates. The best part is it works surprisingly often — and if it doesn’t, so what? Especially considering you can save more than $1,000 with a single phone call.

Remember: Negotiations are all about being polite yet firm. Remind them that you’re a loyal customer and appreciate their service — but you’d really like to have your interest rates lowered to help you pay off debt.

ACTION STEP: Use this script to lower your APR.

Here’s a word-for-word script that many of my readers have used already to lower their interest rates:

YOU: “Hi, I’m going to be paying off my credit card debt more aggressively beginning next week, and I’d like to lower my credit card’s interest rate.”

CC REP: “Uh, why?”

YOU: “I’ve decided to be more aggressive about paying off my debt, and that’s why I’d like to lower the interest rate I’m paying. Other cards are offering me rates at half what you’re offering. Can you lower my rate by 50% or only 40%?”

CC REP: “Hmmm … after reviewing your account, I’m afraid we can’t offer you a lower interest rate.”

YOU: “As I mentioned before, other credit cards are offering me zero percent introductory rates for 12 months, as well as APRs that are half what you’re offering. I’ve been a customer for XX years and I’d prefer not to switch my balance over to a lower-interest card. Can you match the other credit card rates, or can you at least go any lower?”

CC REP: “I see … hmm, let me pull something up here. Fortunately, the system is suddenly letting me offer you a reduced APR. That is effective immediately.”

Repeat this process for any other cards you can, and then move on to my favorite step.

Step 4: Find the money to pay off your debt

One common barrier to paying off debt is wondering where the money should come from. Balance transfers? Using money from your 401k or savings?

These questions are daunting — which is why I want to address two bad options now and give you some good ones:

- Balance transfer. Many people begin by considering a balance transfer to a card wit a lower APR. I’m not a fan of this. Why? Simple: It’s a Band-Aid for a larger problem (typically your spending behavior). Plus the process is very confusing, rife with tricks pulled by credit card companies to trap you into paying more. A better option would just be to negotiate down your APR.

- Using money from your 401k. This is also not a viable solution. Not only do you put your financial future in serious jeopardy by borrowing against your 401k, you’re setting yourself for a bad habit of dipping into these accounts whenever you fall into debt. Plus you’ll be heavily penalized if you withdraw from your 401k before retirement age — losing even MORE money. I repeat, do not use money from your 401k.

Instead, I recommend you try four things:

- Use the cash you’ve freed up from Step 3. You’re paying less in interest now and should use that money towards taking down your debt.

- Set up a Conscious Spending Plan. This is an automated system that lets you know exactly how much you have to spend each month — while also paying off your debt automatically. More on that here.

- Tap into Hidden Income. Through more negotiations, you’ll be able to save hundreds per year on things like cable, cell phone, utilities, car insurance, and even rent. More on that here.

- Earn more money. This is my favorite way of getting out of debt. You can only save so much money — but there’s no limit to how much you can earn. More on that here.

Wipe out your debt — and live a Rich Life

Beating debt isn’t easy — but through a few straightforward systems, you’ll be able to take control of your debt for good and build habits that’ll lead to financial success.

Do me a favor: Write in the comments below one thing you’re going to do TODAY to help get you out of debt. I’d love to hear from you.

Debt reduction: How to get rid of debt forever is a post from: I Will Teach You To Be Rich.