The Envelope System is a great method for saving money.

It works by allocating money for certain categories like eating out, shopping, movies, and so on in envelopes. Once you spend the money in the envelope, that’s it for the month. You can’t spend more.

It’s a great system to use if you’re in debt, because it forces you to be actively aware of your spending — but is it all it’s cracked up to be?

Let’s break down exactly how the Envelope System works, why it’s good, and some of the drawbacks from utilizing it.

- What is the Envelope System?

- Why does the Envelope System work?

- What’s the catch?

- Own your personal finances

What is the Envelope System?

The Envelope System is all about one thing: Becoming more conscious about the way you spend.

It involves a simple four-step process:

Step 1: Calculate your monthly discretionary spending

Your discretionary spending is all the money that’s left over after you pay off the essentials (rent, utilities, etc.).

And it’s simple: Just take your net monthly pay (income after taxes) and subtract fixed payments like:

- Rent

- Mortgage

- Car payments

- Electric bill

- Water bill

- Gas bill

- Cell phone bill

- Any debt (e.g., credit card, student loans, mortgages)

Everything left over is the money you’re allowed to spend on whatever you want for the month.

For example, say your net monthly pay is $3,000. After accounting for your rent ($750 / month) and utilities ($150 / month), you find that you have $2,100 left. Awesome! This means that $2,100 can now be spent on things like eating out and movies.

Which brings us to …

Step 2: Create your spending buckets

So you know how much you can spend. Now it’s time to decide what to spend it on.

To do that, you’re going to create buckets for all discretionary spending you make in a month, such as:

- Eating out

- Going to bars

- Watching movies

- Paying for gas

- Shopping for groceries

- Buying books

There are a lot of different buckets you can create. That’s why I highly suggest you employ my Rich Life philosophy. This is the idea that you should only spend on the things that you love and help make your life rich — while ignoring everything else.

Love buying lattes each morning? Create a bucket for “coffee” or “drinks.”

Can’t help but catch new movies when they come out? Create a bucket for “movies” or “entertainment.”

Easily swayed by your local bar’s special on Jägerbombs? Create a bucket for “bad decisions.”

And if you’re not into any of those things, guess what? You don’t have to create a bucket for them!

Spend about half an hour writing down the buckets you want to devote your spending to. A few I suggest:

- Grocery shopping

- Transportation (e.g. bus, gas)

- Eating out

- Bars

- Entertainment (e.g., movies, concerts, theater)

Once you have your buckets, it’s time to move onto the next step:

Step 3: Put money into physical envelopes

Now it’s time to put the “envelope” in Envelope System.

This means going to your bank or an ATM and getting your discretionary spending in cash. Once you do that, put the cash into physical envelopes dedicated to the buckets you came up with in the previous step.

If you have a bucket for movies, you’d have an envelope labeled “movies” with money inside of it.

You don’t need to use physical envelopes either. One of my friends who started tracking her spending a while back had a great system: She set up a separate bank account with a debit card.

At the beginning of each month, she transferred around $200 in it. So when she goes out, she spends that money. And when it’s gone, it’s gone. It’s a fantastic system that helps her be conscious of what she spends.

If you set up a debit account, be sure to call your bank and tell them you DON’T want them to allow you to spend more than you have in your account (this is known as overdraft protection). If you don’t do this, you might run into a ton of overdraft fees.

(By the way: If you do slip up and find yourself slapped with some fees, here’s a handy guide for getting them waived.)

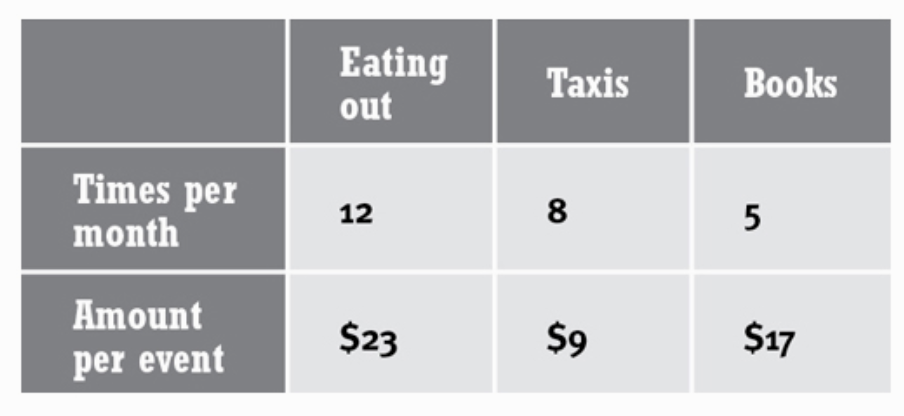

Some of my nerdier friends (aka pretty much all of them) even get more detailed with their system. Here’s a table one of them created:

“Each month, I try to cut the quantity and amount I spend on something,” one friend told me. In less than eight months, he cut his spending by 43%.

Personally, that level of analysis is overkill for most people — BUT it’s a great example of how detailed you can get when you’re conscious with your spending.

Whatever system you decide to use, you just need to make sure to decide how much you’re willing to spend in each category (and that’s all up to you).

Step 4: Spend!

Now it’s time for the best part: Spend your money!

But remember: Once you’ve used all the money in an envelope, that’s it. You’re finished for the month.

The Envelope Method is flexible, though. You can dip into other envelopes if there’s an emergency. However, there will be less money to spend in those envelopes if you do so.

It might take 1 – 3 months of experimenting before you find an envelope mix that works for you — which is fine! Each person is different.

For example, you might find that you don’t use your car as much as you thought, so you have a ton of money left over from your “transportation” bucket. You can allocate that money to another bucket where you could use a little more spending.

After fine-tuning, you’ll eventually find a healthy asset mix that satisfies your Rich Life.

Still have money? Awesome!

So you’ve implemented the Envelope System, found the correct amount of money you want to spend in each bucket, and you still have money leftover?

First off, congrats for being conscious with your spending AND having money to spare. That’s an awesome accomplishment that puts you ahead of the vast majority of people.

Now, you can do a variety of things with that extra money.

If you’re in debt, use that extra cash to pay it down. With your interest rates, any amount of money going toward paying your debt is going to save you a lot more in the future. Be sure to check out our article on getting out of debt fast for more.

If you’re not in debt, you can save that money in a high-yielding savings account toward a money goal. Or you can put the money toward an investment like a Roth IRA.

Why does the Envelope System work?

The Envelope System is great because it leverages a few crucial aspects of human psychology.

A big reason people overspend or don’t save each month is due to the pain of putting money away. This is why doing things like cutting out lattes or skipping out on lunch at your favorite deli is an awful way to save more.

We might do it once or twice — but if we have to make the decision EVERY paycheck, we set ourselves up to fail.

The Envelope System allows us to know exactly how much we have to spend each month. Because of that, we get to spend our money guilt-free.

The system also works well because of cash.

Using physical cash in your transactions forces you to be incredibly conscious with the way you spend. When you watch your dollars go away after buying a coffee, you’re going to be less inclined to spend more of it.

Don’t just take our word for it. We talked to financial therapist and social worker Colleen Lennon on the psychology behind this:

“There’s power in physical money — not just a credit card. I always tell [my clients] to take the money they’re going to spend in a month and put it in different envelopes.

“They’ll always come back the next week and tell me, “I don’t want to touch any of that money! I didn’t order food in. I didn’t go out drinking. I just wanted that money in my envelope. I saved the whole week!

“That’s because they started to respect the money once they can see it.”

So the Envelope System is great — but what are some of its drawbacks?

What’s the catch?

The Envelope System does have a few downsides to it.

If you’re using physical envelopes with cash to allocate your spending, you aren’t going to be able to directly pay for things that require a debit or credit card (e.g., Ubers, Lyfts, online purchases).

You also won’t be able to leverage credit card rewards, which are free perks and benefits such as plane tickets and cash back for spending on things you would have already spent money on.

If you’re using a debit card to track your spending, you’ll have to be much more diligent about your spending. You’ll be much more susceptible to overspending if you can’t see how much you’re spending. This means one weekend could blow your budget for the month.

That’s why the Envelope System is great for a temporary solution if you’re in debt or are working toward a savings goal. Once you’ve gotten out of debt or reached your goal, you can stop using the Envelope System.

Own your personal finances

The Envelope System is great if you want to:

If you want to earn more money so your envelopes get a bit bigger, I want to help you get there.

One of my favorite mantras is simple:

There’s a limit to how much you can save. There’s no limit to how much you can earn.

Once you realize your earning potential is limitless, you can start working towards your version of a Rich Life.

That’s because cutting more spending isn’t really feasible for some people — especially if you’re living paycheck to paycheck. However, you can circumvent this issue by earning more.

I want to show you two strategies you can use to earn more:

Negotiate a raise

If you already have a job, it’s a no-brainer to negotiate for a raise.

However, it does take some careful planning. Most importantly, you need to demonstrate your value to your employer.

That’s because getting a raise isn’t about you. It’s about what you can do for your boss.

To help you do exactly that, be sure to download my Ultimate Guide to Getting a Raise and Boosting Your Salary. In it, I’ve included my best systems on:

- How to get paid what you’re worth. Learn how to land a promotion and a raise that could be worth hundreds of thousands of dollars over your lifetime, or more. Get the step-by-step process for negotiating a raise — plus word-for-word scripts you can use.

- Salary negotiation tactics. What are the signs that show you’re worthy of more respect, attention, and income? Learn these three salary negotiation tactics to multiply your chance of getting a raise and prevent social mistakes from holding you back.

- Beyond salary. I’ll share even more of my best material on establishing a salary range, getting additional vacation days or overcoming your boss’s most common objections.

Earning more money doesn’t have to happen inside of your job either — which brings us to …

Starting a side hustle

This is one of my favorite ways to earn more money.

In a week, you can start a freelance business that helps you generate cash outside of your normal work. Not only that, but you can scale your side hustle to earn as much as you want.

That’s why my team and I have worked hard to create a guide to help you earn more today:

In it, I’ve included my best strategies to:

- Create multiple income streams so you always have a consistent source of revenue.

- Start your own business and escape the 9-to-5 for good.

- Increase your income by thousands of dollars a year through side hustles like freelancing.

Download a FREE copy of the Ultimate Guide today by entering your name and email below — and start earning more money today.

How to use the Envelope System to save hundreds per month is a post from: I Will Teach You To Be Rich.